Q&A with Guy Carpenter: Are reinsurers meeting the needs of cedants?

In this extended Q&A, Guy Carpenter’s co-heads of cyber, Erica Davis and Anthony Cordonnier, spoke to CyberInsurer.com about whether the cyber reinsurance market is meeting the needs of cedants, current trends in rates, the availability of coverage, and how comfortable the cyber reinsurance market seems to be with the peril.

⦁ To what extent is the cyber reinsurance market meeting the needs of cedants? Where is it falling short?

Cyber insurers generally have access to capacity from reinsurers to support their expansion in the class. While capacity is still under some pressure, it remains available depending on terms.

The growth of cyber market is driven by the digitisation of the economy, increasing product penetration, the evolution of threat landscape, increasing sophistication of regulation, changing levels of support from existing players and the entry of new underwriters to push the offering forward.

More purchases and additional capacity are sought in the marketplace, as awareness of systemic cyber events grows and cyber portfolios increase in size, largely driven by the current pricing environment.

Underlying pricing has increased due to market conditions and lack of new capacity. Beyond pricing, there is heightened expectations around risk controls, limits, management strategies in effect and greater emphasis on technical acumen.

Many carriers are reducing capacity exposed. Incumbent reinsurers, due to capacity constraints, may look to reallocate capacity to perceived higher-margin deals. Some carriers are scaling back ransomware-related coverages (or not offering coverage at all) for clients that don’t have adequate controls.

Some reinsurers have increased monetary capacity deployed in line with market demand, while others have maintained or even reduced monetary aggregates deployed.

In order to position clients for success, it is critical to engage year-round on data quality, market behaviours and understanding the impacts recent underwriting strategies have had on portfolio performance.

Exposure accumulation remains a concern across the cyber sector and new capacity must continue to enter the market in order to meet demand. Guy Carpenter is also sourcing cyber reinsurance capacity globally to expand the panels on growing client portfolios or to fill gaps of those markets with shifting appetites.

Anthony Cordonnier and Erica Davis

⦁ How available are excess of loss (XoL) covers?

New placements are coming to market, and additional capacity is being sought on existing placements. This is driven, of course, by the underlying growth of the cyber insurance market, as well as an increased awareness of the potential impact of systemic cyber events.

The cyber reinsurance market has hardened quickly, with a shift in pricing as rates on line (ROLs) have seen double-digit increases. The last renewal cycle, however, has shown a decelerating trend of price increases.

Deterioration of loss ratios industry-wide has altered reinsurer perspective on attachment point, leading to a strong preference for attaching well above 100%. Attachment points are expected to remain more stable in view of the improvement of underlying portfolios.

Aggregate capacity is being closely managed by reinsurers, with new deals facing a much higher bar to attract sufficient capacity

⦁ And what are the trends in quota share (QS)?

Average ceding commissions have stabilised, after a trend of reductions in the last two renewal cycles. Renewals were primarily flat, with newer quota shares more closely scrutinised.

The limited availability of capital has continued to put downward pressure on loss ratio/aggregate caps. Uncapped quota share treaties and treaties with event caps are now very rare.

Across Guy Carpenter’s client base, more than half of cyber QS buyers now also buy aggregate stop-loss capacity.

⦁ What are the current trends in reinsurance rate movements? How long can we expect the cyber reinsurance hard market to persist?

Guy Carpenter's estimated calculation for the cyber/blended (errors and omissions (E&O)/cyber) market is $10bn in gross written premium (GWP) globally at year-end 2021, with a full-year rate increase of 78%.

In the direct market, Marsh’s US client base shows:

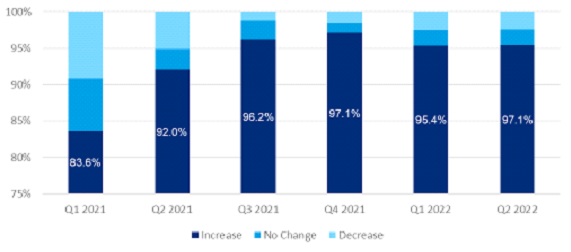

⦁ in Q2 2022, cyber rates increased by an average of 78.8% down from 109.9% in Q2.

⦁ This compares to an average increase of 35.1% on renewals in Q2 2021.

⦁ 97% of insureds received a rate increase in the Q2 2022. (see figure 1)

This continues the trend of rate increases seen over the last eight quarters.

Rate increases for 2022 are expected to be heavier in Q1/Q2 than in Q3/Q4 due to significant pricing corrections having been applied from Q2/Q3 2021.

We expect that the primary market’s actions (both from a rating and underwriting standpoint) and its subsequent profitability turnaround will lead to greater comfort from reinsurers, which will, in turn, attract additional capital to the class and relieve some pressure on terms and conditions in the coming reinsurance cycle.

⦁ What are you hearing on the ground about new capacity or new entrants to the market? How much is the hard market likely to tempt carriers into cyber reinsurance?

New capacity has come to market recently, both in the traditional and non-traditional space. This comes with a degree of product innovation, too—for example, with event excess of loss covers, which had become very rare in the cyber reinsurance market.

We are also seeing existing players increasing their appetite, although larger reinsurers are growing at a faster pace than their peers.

Reinsurers who had observed cyber market dynamics from the sidelines are acknowledging these underwriting shifts and now signalling interest in entering the market.

⦁ How comfortable are reinsurers currently with cyber risk?

Reinsurers are concerned about frequency and severity of individual losses (particularly driven by ransomware trends), although this has recently stabilised.

Reinsurers also scrutinise the impact that common vulnerabilities can have on loss aggregation, as well as the ability of cyber attacks to cause a large loss on a single risk.

This is supported by the growth of a distinct skillset within reinsurers, with an increase in the number of teams being fully dedicated to writing cyber reinsurance.

Reinsurers are increasingly licensing vendor aggregation models in addition to building their own proprietary scenarios.

The vast majority of reinsurers are seeking to build sustainable cedent relationships and are committed to the cyber class of business in the long term.

Are there any other interesting trends in the cyber reinsurance market that you think a specialist audience ought to be aware of?

War exclusions, long considered to be an area of opportunity for better clarity in the cyber market, came under increased scrutiny in 2022 given the Russia/Ukraine conflict.

Additionally, the Lloyd’s Market Association released a series of cyber war clauses in Q4 2021.

Many insurers are reassessing their current policy war wordings to determine if clarification is needed based on these developments. We expect further evolution on this issue in the coming months and will work with our clients to ensure alignment of intent with their reinsurance partners.